LISTEN TO THE ARTICLE

At the outset, it is worth distinguishing the two automatic tax information exchange initiatives.

FATCA, the acronym for the US’ Foreign Accounts Tax Compliance Act 2010, is an initiative of the United States Government. Via bilateral agreements with other governments the IRS receives annual reports containing specific details of financial accounts held by US tax residents outside of the US. The US Treasury website shows that currently 113 such intergovernmental agreements (IGAs) are in place, of which one hundred are operational. Five of the GCC countries: Bahrain, Kuwait, Qatar, Saudi Arabia and the UAE have Model 1 IGAs in effect with the United States. Oman does not yet have an IGA with the US.

The Standard for Automatic Exchange of Financial Account Information in Tax Matters, more popularly known as the Common Reporting Standard (CRS), is a multilateral initiative developed by the OECD. Like FATCA, it has objective of facilitating cross border tax compliance. The United States is not part of the CRS initiative. The CRS initiative enables governments that have signed onto a multilateral accord for tax cooperation, to share financial account information of relevant taxpayers with each other. The latest information from OECD website shows that 120+ jurisdictions have signed onto the multilateral accord, including all six GCC countries.

The actual financial account information sharing for CRS is activated between signatories to the multilateral accord on a bilateral basis. According to the OECD website as at 8 Jan 2024, the UAE has 82 such partners.

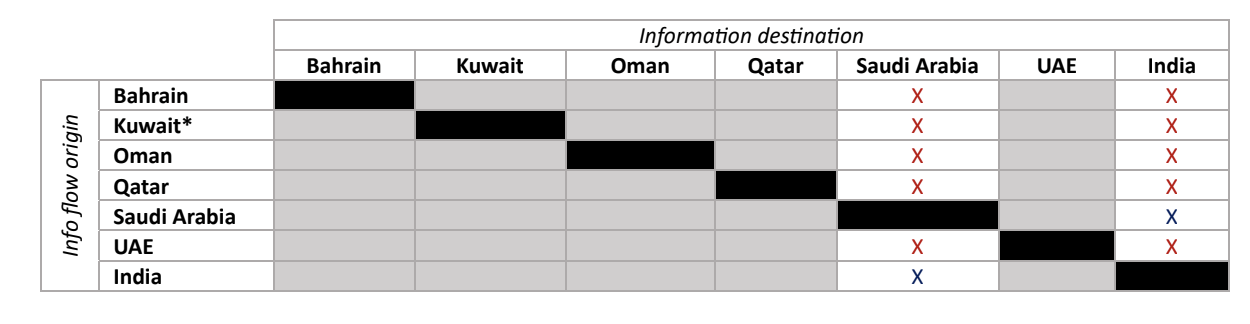

CRS Information sharing across GCC countries and between GCC and India illustrated below.

Source: Exchange relationships - Organisation for Economic Co-operation and Development (oecd.org)

--- information flow is one way (RED) -- information flow is reciprocal (BLUE) *according to the OECD 2023 AEOI Peer Review Report, Kuwait has suspended its CRS information exchange pending updates to its implementation framework.

--- information flow is one way (RED) -- information flow is reciprocal (BLUE) *according to the OECD 2023 AEOI Peer Review Report, Kuwait has suspended its CRS information exchange pending updates to its implementation framework.

To activate the international tax information sharing agreements (Model 1 IGA and CRS) internally, governments typically implement ratification laws where these do not already exist. The implementing laws, amongst other obligations, mandate designated domestic reporting financial institutions (RFIs) to collect information on all reportable accounts they hold and file such details (as per the governing domestic regulations) with a relevant domestic competent authority.

For most CRS signatories, the sifting of the information for onward transmission to partner jurisdictions is carried out at the level of the domestic competent authority. The information shared is the financial account information relevant to an identified tax resident of the government with whom the information is shared.

Understanding which countries have signed IGAs with the US and signed onto CRS is important in light of the treatment mandated for accounts which are owned by tax residents of countries that are not signatories to these initiatives. Such accounts are generally deemed to be reportable.

Benefits of complying with FATCA & CRS

Both initiatives provide market access incentives for participating countries and cooperating national entities within their borders. The applicable benefits are generally a matter of the tax laws of the receiving jurisdiction.

Additionally, the FATF 40 recommendations recognize tax evasion as a predicate offence for money laundering. A robust global tax information exchange network significantly reduces opportunity for this type of ML.

Implementing FATCA Model 1 IGA & CRS

Implementing legislation/regulations impose compliance obligations on RFIs to conduct due diligence, maintain records, file related returns with designated domestic authorities. They also provide enforcement mechanisms to ensure compliance with these obligations.

RFIs are entities and not individuals. As a first step therefore, to determine whether an entity is an RFI (and what type – custodial, depository, specified insurance company or investment entity), an analysis in the form of an entity classification self-assessment must be carried out for FATCA and for CRS.

This initial entity classification review facilitates the establishment of the database of RFIs that have mandatory registration and other compliance obligations with the relevant authorities.

Typically, financial service provider licensing/registration applications incorporate requirements for the applicant to indicate its FATCA and CRS classifications.

In the case of Investment Entity Type B, however, the designation of financial institution is not based on the provision of a prescribed service, but rather on income and asset activity and the management of the related financial accounts in a prior period.

The entity classification self-assessment is an important review and must be undertaken against prescribed FATCA criteria and CRS criteria. While the entity classifications for both FATCA and CRS are broadly similar, there are some distinctions in the case of an Investment Entity Type B.

The relevant domestic laws implementing the initiatives will specify the circumstances where exemptions from reporting exist for each initiative. However, there are more exemptions from reporting under FATCA than under CRS. This is due in part to recognition given by the IRS to circumstances where the information to be reported is being supplied to the IRS by other means e.g. IRS concept of deemed registered and certified financial institutions.

Where there are no accounts to be reported, typically the law requires the RFI to file a NIL report.

In the case of FATCA there is also the added requirement for RFIs to be registered with IRS and have a Global Intermediary Identification Number (GIIN). GIIN registration can be carried out online via the IRS portal.

As an ongoing governance matter, it is also a good rule of thumb for entities to conduct annual entity classification self-assessments since a change in circumstances during a calendar year may alter the conclusion of a prior assessment. For example, a change in circumstances may occur with BOs & controllers, business activities, clients, income/revenue sources and thresholds, and business locations, amongst other considerations.

Internal FATCA and CRS compliance frameworks

RFIs must implement and maintain FATCA and CRS compliant policies, procedures, and internal systems. This starts with determining which accounts are reportable for each initiative. The regulatory and competent authorities issue notifications on the timeframes for submitting reports.

Reportable accounts are those which must be declared annually to the competent authorities. They are determined primarily on based on account type, threshold values in the case of some legacy accounts, and account holder tax residence indicators. Onboarding documentation for each client should contain the relevant current details supporting each determination.

Sophisticated investors frequently have multiple nationalities and/or tax residences. Further sophisticated investment structures will involve multiple jurisdictional tax and reporting considerations.

It is worth noting that because FATCA provides more scope than CRS to exclude certain financial accounts from being reported, this may result in the situation where an RFI must report accounts for CRS, but not for FATCA.

Finally, when implementing compliance frameworks, a certain caution is advised regarding legal definitions and language usage as these are not necessarily uniform across all jurisdictions. For example, the W-8BEN-E requires a Chapter 3 status selection, one of the options for which is a “private foundation”. This has given rise to confusion in cases where an entity is registered as a “foundation” in a country outside of the US, with closed membership that is deemed private in the jurisdiction of incorporation. However, the concept of a private foundation in the W-8BEN-E form is based on US Tax law with a different connotation.

More articles around FATCA

FATCA: Small / Limited Scope UAE Financial Institutions (FI) Exempt From Reporting*

UAE Non-Reporting Financial Institution for FATCA & CRS Purpose

Disclaimer: Content posted is for informational & knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. The view/interpretation of the publisher is based on the available Law, guidelines and information. Each reader should take due professional care before you act after reading the contents of that article/post. No warranty whatsoever is made that any of the articles are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.

Contributor

Rowena Bethel is a Consultant/Advisor on FATCA and CRS compliance with

Ryja Consulting, Dubai, UAE. She is former head of the International Tax

Cooperation Unit in a Caribbean IFC and former country representative at the

OECD Global Forum on Transparency and Exchange of Tax Information. She

was a peer review assessor for the OECD Global Forum EOIR round of

assessments and also served as a member and rapporteur on the UN Committee

of Experts on International Cooperation in Tax Matters.

Related Posts

@@PLUGINFILE@@/FATCACRS%20Reporting%20Obligations%20Of%20UAE%20Investment%20Entities.mp3 ...

Read More

@@PLUGINFILE@@/FATCA%20Small%20%20Limited%20Scope%20UAE%20Financial%20Institutions%20%28FI%29%20Exem...

Read More

All UAE financial institutions (FI), defined as such for FATCA and CRS purposes, are Reporting Fin...

Read More