LISTEN TO THIS ARTICLE

In an increasingly digital and interconnected world, traditional tax rules struggle to keep pace with the global nature of businesses. The Organization for Economic Co-operation and Development (OECD) recognized this challenge and proposed a two-pillar solution to address tax challenges arising from the digitalization of the economy. Let’s understand what Pillar One and Pillar Two means.

Pillar One: Redefining Tax Allocation

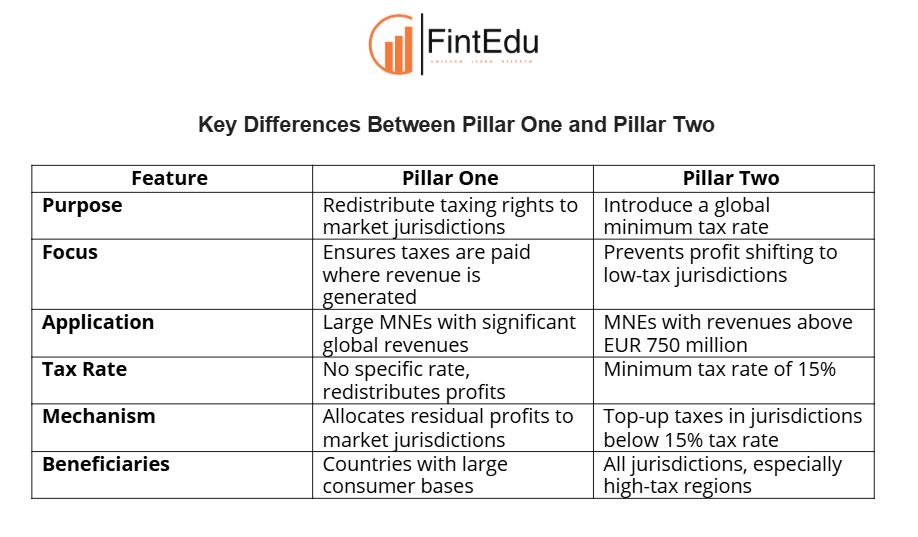

Pillar One establishes new rules for allocating a portion of residual profits from multinational enterprises to the countries where their customers or users are located. This applies regardless of whether the company has a physical presence in those countries.

- Scope: Pillar One applies to large MNEs with global revenues exceeding a defined threshold (e.g., EUR 20 billion) and profitability above a certain level.

- Profit Allocation: A portion of residual profit (profits exceeding a standard return) is allocated to market jurisdictions based on sales.

- Objective: Address the tax challenges posed by highly digitalized businesses that generate significant revenue in countries without maintaining a physical presence.

- Example: A global tech company earns substantial revenue from users in Country A through digital services. Despite no physical office in Country A, a share of its profit is taxed there.

Pillar Two: Establishing a Global Minimum Tax

Pillar Two aims to ensure that large MNEs pay a minimum level of tax globally, regardless of where they operate, by introducing a global minimum tax rate.

Definition:

Pillar Two creates a framework for a global minimum effective corporate tax rate (set at 15%), ensuring that MNEs pay at least this rate in every jurisdiction where they operate. If they pay less, other countries can collect the difference through a top-up tax.

- Scope: Applies to MNEs with annual revenues above a threshold (e.g., EUR 750 million).

- Minimum Tax Rate: Sets a global minimum effective tax rate of 15%.

- Top-Up Mechanism: If an MNE pays less than 15% tax in a jurisdiction, other countries can impose additional taxes to meet the minimum.

- Objective: Prevent profit shifting to low-tax jurisdictions and ensure fair taxation.

- Example: If a company shifts profits to Country B with a 5% tax rate, another country (e.g., the headquarters’ country) collects the additional 10%.

Conclusion

OECD’s Pillar One and Pillar Two frameworks represent a significant shift in global taxation policies. While Pillar One focuses on fairness by taxing companies where their consumers are located, Pillar Two ensures a level playing field by setting a floor on tax rates globally. Together, they aim to create a more equitable and sustainable tax environment.

Contributor

Related Posts

UAE, 02 July, 2026: The Federal Tax Authority (FTA) has released its 2025 Annual Report, highli...

Read More

UAE, 02 July, 2026: The Federal Tax Authority (FTA) has expanded the list of construction expen...

Read More

Why Internal AML Audits MatterAn AML programme should not only exist on paper—it should work effec...

Read More