Value Added Tax (VAT) in the UAE can feel confusing, especially when it comes to schools and universities. Some things are taxed, some are not, and some depend on small details. This article breaks it all down in plain, everyday language so you know exactly what is taxed and what isn't.

The Basic Idea: Two Boxes to Tick

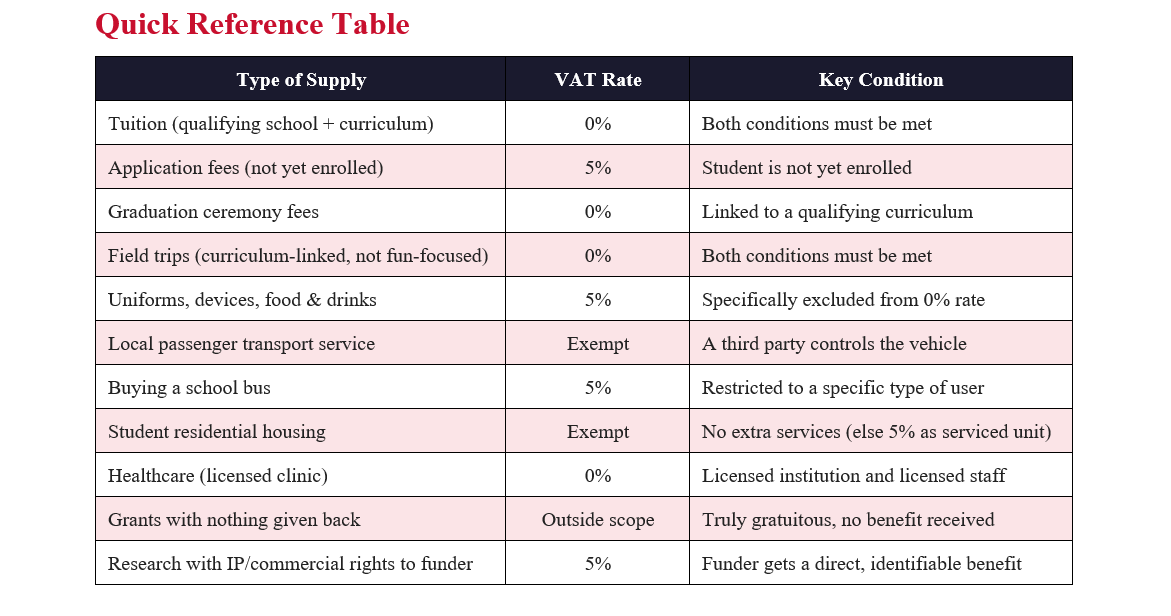

Not every school or course automatically gets a VAT break. For education services to be "zero-rated" (meaning 0% VAT instead of the usual 5%), two things must both be true at the same time:

• The institution is a "Qualifying

Educational Institution" recognised by a government authority, or (for

higher education) either government-owned or getting more than 50% of its

yearly funding from the government.

• The course follows a "Qualifying

Curriculum" one that is officially recognised by the government body in

charge of education in that area.

If either box is not ticked, the service is taxed at the standard 5% rate. This 0% rule is treated as an exception, so it's applied strictly both conditions must be clearly proven, often with documents like a licence or funding records.

What Actually Counts as "Education"?

The law does not spell out an exact definition of "education." It's simply understood in the normal sense: teaching, training and learning that happens in places like schools, colleges and universities, aimed at building knowledge and skills.

Gets 0% VAT (Zero-Rated)

Tuition delivered by a qualifying school or university, teaching a curriculum that is officially approved. Both conditions from the section above must be met together.

Gets 5% VAT (Standard-Rated)

• Private tutoring or home-schooling

given by people or businesses that are not qualifying institutions

• Diplomas or courses that don't lead

to a recognised degree

• Skills training at private training

centres

• Education management services

provided by outside companies

What About Books, Trips and Extra Activities?

Goods and services sold by a qualifying school can also be tax-free, but only if they are a necessary and integral part of delivering the education, not just something extra sold on the side.

Usually Tax-Free (0%)

• Printed

or digital textbooks tied to the approved curriculum

• School

trips that are clearly linked to what's being taught, and not mainly for fun

• Extra

activities like football training, as long as there's no extra charge for them

• Re-registration

fees for students already enrolled

• Special

needs support that is part of the curriculum

Usually Taxed at 5%

• Items

sold to people who aren't enrolled students

• School

uniforms and required clothing

• Devices

like tablets or laptops

• Food

and drinks, including vending machines

• Extra

activities that cost extra money

• Trips

that are mostly for fun, like a waterpark or amusement park

Common Situations Explained Simply

Application and Registration Fees

If a student hasn't been

accepted yet, the application fee is taxed at 5%. But if they get in and the

fee is later counted toward their tuition, the school should cancel the

original tax invoice (with a credit note) and issue a new zero-rated invoice.

School Fundraisers

A cake sale to raise

money for a new library is normally taxed at 5%, because it's a fundraising

activity, not teaching. But if it's something like a concert that is actually

part of a student's official exam, it can be tax-free.

Field Trips

A trip only avoids tax if

it is closely tied to the curriculum and not mostly for entertainment. A

waterpark trip is taxed. A museum visit connected to an art class is not.

Graduation Ceremonies

Fees for graduation and

certificates linked to an approved curriculum are tax-free. Basic refreshments

served at the event don't change this.

Beyond the Classroom: Housing, Buses and Health

Student Housing

Renting out a residential

building is generally exempt from VAT. But if the school also throws in

services like room cleaning, laundry, or meals, it becomes a "serviced

unit" and is taxed at 5% instead. Shared spaces like lounges and general

cleaning don't count as extra services.

School Buses

Paying for a transport service where someone else drives and owns the bus is exempt from VAT. But if the school buys or leases its own bus, that purchase is taxed at 5%, because school transport isn't treated as general public transport.

Health Clinics

A clinic run by a

licensed school with licensed doctors or nurses can be tax-free. But admin

charges, like opening a medical file or an annual health fee, are taxed at 5%.

If an outside healthcare company supplies services to the school (rather than

directly to students), that's taxed too.

Online and Distance Learning

Pre-recorded courses that

run automatically, with no live interaction, count as "Electronic

Services." But if students can actually talk to a tutor or get personal

help, it's not treated as an Electronic Service. This distinction matters a lot

for foreign providers, since it can affect whether they need to register for

UAE VAT.

Money Coming In: Grants, Scholarships and Research

The key question here is simple: does the person paying get something valuable back in return?

• Third-party tuition (parent, employer

or government pays): treated the same as if the student paid tax-free if the usual conditions are met.

• Scholarships from the school: treated

like a discount, so VAT is charged only on the smaller, discounted amount.

• Pure grants or donations with nothing

given back: outside the scope of VAT entirely.

• Grants where the donor gets

something, like naming rights: this counts as payment for a service, so VAT

applies.

• Research done for commercial reasons,

or where the funder gets shared rights to the results: taxed at 5%. Renting out

labs or facilities to outsiders is taxed too.

Claiming Back VAT on Purchases (Input Tax)

Schools can only claim

back the VAT they paid on things they bought if those purchases were used to

make taxable (5%) sales. VAT spent on exempt activities, like plain residential

accommodation, can't be claimed back.

If a school has a mix of taxable and exempt income, it needs to work out a fair split (apportionment) for shared costs. There's also a special "Capital Assets Scheme" for big-ticket items, buildings or other assets worth AED 5,000,000 or more, used for 10+ years (buildings) or 5+ years (other assets).

• Events like National Day celebrations

or recruitment days: VAT is claimable as a normal business cost. But VAT on

pure entertainment, like an iftar dinner, cannot be claimed.

• Buying or renting a school bus: VAT

is charged at 5% on this. If that bus is then used to provide exempt local

transport, the VAT paid can't be claimed back.

• Staff accommodation: VAT can be

claimed only if it's legally required under UAE labour law, written into an

employment policy, or genuinely necessary for the employee's job ideally all

three.

The Bottom Line

VAT on education in the

UAE comes down to two simple checks: is the institution officially qualifying,

and is the curriculum officially recognised? Once you know that, most other

questions about trips, fees, buses, housing

or research fall into place using the same logic: is it genuinely part of

delivering education, or is it something else attached to it?

Because the rules have many small exceptions, it's worth getting professional advice for anything unusual or high-value.

Disclaimer: Content posted is for informational and knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. The view/interpretation of the publisher is based on the available Law, guidelines and information. Each reader should take due professional care before you act after reading the contents of that article/post. No warranty whatsoever is made that any of the articles are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.Contributor

Zubair Khan – Corporate Trainer & Finance Expert

Based in Dubai, UAE, Zubair Khan is a Chartered Accountant (CA) and Partner – Taxation at RHMC with 14+ years of experience delivering corporate training for mid to top management, finance professionals, and business leaders. He specializes in IFRS, UAE Corporate Tax, VAT, financial statement analysis, and finance for non-finance professionals.

He has trained professionals across industries, including Louis Vuitton, Imdaad, Strata Manufacturing, JCDecaux, and more. Zubair combines technical expertise with practical, real-world applications to enhance strategic decision-making and regulatory compliance.

Qualifications: CA (ICAI), Diploma in IFRS (ACCA), B.Com

Previous Roles: Corporate IFRS Coach, Educator at Unacademy, BB Virtuals, Lakshya CA Campus.

Related Posts

Executive Summary The Federal Tax Authority (FTA) has released an updated version of its...

Read More

IntroductionThe UAE introduced a federal Corporate Tax regime under Federal Decree-Law No. 47 of 202...

Read More